What is Fintech and DeFi? Differences, Benefits, and Risks

Having been in the space since 2017, and working in-house for an EVM-ready Layer-1 and also a neobank with a self-custody wallet has allowed me to really understand this industry and see it through a special lens.

“The entire industry stems from finance, which has been around since 3000 BCE in Mesopotamia. "Finance" actually derives from Old French, Medieval Latin "finis", to settle and end a debt.”

In my opinion, Financial Technology (Fintech) and DeFi (Decentralized Finance) are intertwined, though they have distinct differences.

When it comes to fintech vs DeFi, one runs through banks rails, the other runs on blockchain code.

Fintech covers essentially everything in the financial world today. By default, most bank accounts are associated with some sort of technology stack to sustain today’s needs.

Rarely do you see someone paying with cash nowadays, not to mention the tax mess it comes with.

DeFi, on the other hand, is just a growing part of fintech that the crypto industry developed, and as you guessed, it involves crypto.

What Is Fintech? Origin story

In 1950, most of the fintech infrastructure began with the credit card, introduced by what was then a little-known company called Diners Club.

Pretty funny, no? The world of credit cards started at a regular NYC diner, not far from your local Steak 'n Shake.

How Fintech Works

Fintech itself has way too many branches to simplify. In short, it is the blend between technology and the financial system.

From a banking and infrastructure standpoint, crypto simplifies the factoring and trading side of things, enabling transactional and custodial features at a cheaper, faster rate than usual.

On the other hand, one needs to realize that crypto and blockchain are just optimized tech stacks for particular use cases. And inevitably, more tech and innovation will follow.

Common Fintech Examples

- Banking apps

- Payments

- Neobanks

- Lending and credit

- Investing and wealth management

- Personal finance management (PFM)

- Insurtech (insurance technology)

- B2B fintech and infrastructure

- Crypto and digital assets

9 Best Fintech Companies in 2026

Stripe

Ramp

Plaid

Chime

Revolut

Nubank (Nu)

Mercury

Klarna / Affirm

Robinhood

What Is DeFi? The early days

So what is DeFi, exactly? At its core, DeFi relies on decentralization to mimic the current financial system, from banking to private equity, lending, and beyond.

How DeFi Works

Decentralization, paired with smart contracts, is the backbone of DeFi.

A smart contract, in simple terms, can be imagined as a set of rules that cannot be edited. That’s the nature of a smart contract and how it differs from Web2 code.

Some call this programmable money. Once the smart contract goes on main net, it cannot be changed.

Decentralization also plays an important role, as it enhances transparency by leveraging the public ledger.

Common DeFi Examples

- Lending

- DEXs

- Staking and liquid staking

10 Best DeFi Companies in 2026

Lido

Aave

EigenLayer

Uniswap

Sky (formerly MakerDAO)

Morpho

Curve

Jupiter

Pendle

GMX

Fintech vs DeFi: Key Differences

Centralized vs Decentralized

As mentioned before, the main point here is how keys are handled in centralized and decentralized systems.

A common bank, for instance, will hold your assets, and you are at their will. Meaning that if they decide to change something in the terms and conditions, or there is a local jurisdiction change, you must comply to handle your assets.

In terms of decentralization, your keys belong to you and only you. Your account cannot be accessed or recovered without the secret phrase or keys. Therefore, folks who use a decentralized non-custodial wallet can operate as their own bank.

Custody: Who Holds Your Money

When it comes to traditional banking, for instance, they hold your assets in custody. What seems like a common need really relies on trust that these entities have been safe and readily available for you at all times. If you want a bank that works with crypto, we covered the top crypto friendly banks worth considering.

If you need to pull cash from an ATM late at night or need a payment approved quickly, Web2 banking still delivers beyond crypto.

The simple part that is forgotten is that paper cash, or digital cash, as we know it today, is just another “thing”, another asset.

Crypto, on the other hand, can only hold digital assets, crypto, NFTs, or whatever the fascinating world of Web3 has to offer.

No Recovery: The Custody Trade-Off

If you are coming from the classic world of fintech, with a typical Chase or Bank of America bank account, for instance, getting customer is a different story.

If you are locked out from your bank account, you are always one call away from a 24/7 call center. Which in my opinion, even as super crypto fan, is the best service ever.

A no brainer to be honest.

Crypto does not give you a second chance if you lose your keys or get drained by a hacker for interacting with a fishy crypto service.

Just like crypto might seem sophisticated, understand that there are malicious actors as technical as the good guys. These guys work to scam folks at mass, and if you are not careful, you could be next.

My recommendation is to always work with tools that are well established, or simply open a new wallet that you do not care if it gets drained or not. The latter is a good practice to test new things out.

ZackXBT is a good person to contact if you get drained and it seems impossible to recover your assets.

Just take into account that the line of folks asking for his help is massive. Unless you are talking about recovering a serious amount of money, then it’s probably better to ask elsewhere or just move on.

This is quite the issue to still fix in crypto. Single sign on, and KYC’d solutions are entering the space. Something to keep an eye on, and certainly test.

Transparency and Auditability

In terms of transparency, banking, for instance, offers visibility to the consumer in the form of a bank statement, along with financial reports for investors, and aligns with compliance.

How DeFi Transparency Differs from a Bank Statement

When it comes to showcasing exact factoring and tracing, DeFi has the edge.

Blockchain technology delivers a unique value proposition by delivering live data at all times.

In classic fintech, banking for instance, can you pull someone else's statement without them being by your side? The answer is not necessarily.

In DeFi, you are one scanner away from seeing the insights you need. Etherscan, Solscan, Near Blocks, are all great examples. Understanding a contract address is also key before interacting with any of these tools.

If you are a bit confused at how scanners work, or what you can do with them, it’s totally okay. The reality is that these tools could be more straightforward, but each smart contract is different.

Remember, you are always one video tutorial away, or a quick Discord/Telegram chat from understanding or executing your objective.

Regulation and Governance

It really depends on what type of fintech service we are talking about. For instance, banks and neobanks with a paired bank charter, meaning they answer to the FDIC and the OCC.

On the other hand, Web3 offers fewer jurisdiction challenges in contrast to Web2 and traditional asset management, for retail or private ops. DeFi is a permissionless system. No approval needed to participate.

Decentralization again gives the chance to also introduce Decentralized Autonomous Organizations (DAO) structures.

These are not unlike a community takeover, where token holders vote on the direction of a project.

These are typically handled through a voting system that includes asset holders. Once decisions are made, they are programmed in smart contracts to execute.

Is DeFi Part of Fintech?

Yes, all things crypto, blockchain, and Web3 are under the fintech umbrella.

Benefits and Risks

Why Fintech Appeals to Mainstream Users

It’s simple. Fintech helps an average Joe like me to transact freely with simpler accounting, billing, and checkouts.

Instead of walking with a pile of cash and its consequences, it’s easier to carry a card or an NFC-ready phone, plain and simple.

For the unbanked, fintech apps are the easiest on-ramp to a first account as long as you KYC and have a local address, a key for financial inclusion.

Why DeFi Appeals to Crypto-Native Users

The main appeal to me comes from crypto being an asset that is easy to transact globally.

Also, in a scenario where countries suffer from financial instability, crypto can be one of the best sources to hedge against inflation scenarios and jurisdiction changes.

A close friend of mine got locked out of his exchange once they found out he had a Venezuelan passport, as he moved to a country in the EU that had specific requirements.

The cool part here is that he could still move his wallet assets due to decentralization. No country or jurisdiction has ever come close to blocking access to blockchains.

You can always recover your wallet with a wallet that works in your new country or simply interact with the smart contract to move it elsewhere, through scanners, Etherscan, or Solscan, for instance.

Risks Unique to Each

In my opinion, risks differ.

The jurisdiction part of the current banking world can impact your bottom line. People tend to forget that banks are businesses, and like in any industry, they are subject to local jurisdiction and compliance changes.

For the most part, people do not even think about banking or how it works because a single transaction, at its core, gets marked up so low that the consumer does not really notice.

DeFi-Specific Risks: Smart Contracts, Rug Pulls, and Lost Keys

Smart Contracts differ per developer.

Although smart contracts deliver unique workflows, most are almost identical. An NFT smart contract is pretty much a 1:1 copy of code that was shared in GitHub anyhow.

The same goes for tokenized, digital assets. Most run on the same handful of audited smart contract templates.

Therefore, the hard part is understanding the name of each smart contract function.

You can call these functions for a very small amount, and execute certain things.

The big picture here is that this is how smart contracts get hacked or exploited. Once the hacker sees the entry, he does not even engage with the front end UX/UI, they simply call the contract at its core.

This is also how bundling in crypto gets weaponized by bad actors executing multiple transactions at once.

When it comes to rug pulls, which happen often, keeping an eye on scanners can often do the trick.

You can see when certain wallets start pulling liquidity, or how wallet networks engage if outflows span out of control.

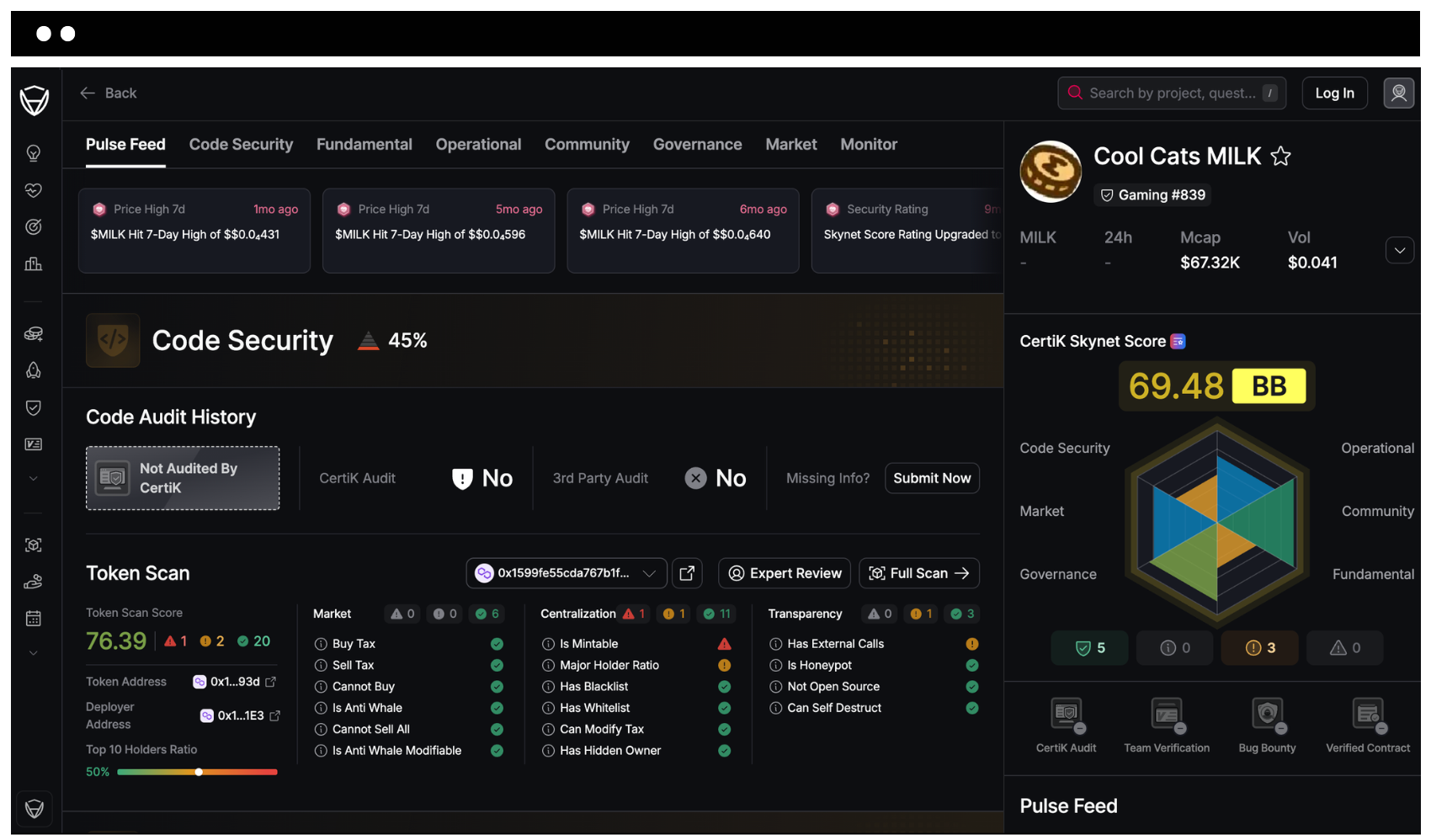

Arkham or Certik Skynet, are great spots to see how this all breaks down. In our contract address (CA) piece, we expand on this tools.

Lost keys seem like a small thing to mention, but please remember that there is no DeFi tool you can interact with without a non-custodial crypto wallet.

Fintech on the other hand is custodial, and offer a better customer support, which means there is no way of losing access to your assets.

Can Fintech and DeFi Work Together?

Yes.

They can either work alone or in tandem.

The Convergence: Fintech Adopting DeFi Rails, DeFi Adopting KYC

Fintech on the backend, has very little room to do much more than adapting the already optimized DeFi rails.

Blockchain technology is being introduced at all levels of the current banking and private finance world.

The whole reason is that at its core, blockchain is cheaper, faster, and more transparent than fintech.

Is DeFi part of fintech? Yes, it's a subset, not a separate vertical.

DeFi adopting KYC is by far one of my favorite updates happening across Web3. Just because KYC gets introduced, it does not mean it will be the ultimate requirement for users.

Non-KYC and KYC’d customers can, and will coexist. For the latter, there are interesting security features that help protect consumers, and also streamline taxable requirements.

Conclusion

Pick your favorite fintech or DeFi tool that matches your needs. Pay attention to what you use in the space.

Is it lending or staking? Perhaps exchanges for trading? If DEXs are your thing, check out how to pay for DEX listings to get your token seen. Trading digital assets? Or as simple as collecting NFTs and crypto art?

At the end of the day, you have to pay attention to what works for you, because chances are, numerous folks are sharing your same interest.

Chime and SoFi, for instance, have done a great job in fintech.

Companies like Uniswap or Phantom are leading the pack in their categories.

If you see something that is working for others, give it a shot. Because most of these tools just require $5 to test out. If you are new, give yourself a day, or even weeks, to understand what you are doing.

No matter what I write, I trust your best judgement will always win. If you see anything cool in the space, do not hesitate to let us know.

Always be curious and wary in the wild world of crypto, and enjoy the ride.

Disclaimer: Some links in this post are affiliate links. When you click through and make a trade or sign up, we may earn a small commission at no extra cost to you. We only recommend platforms and tools we actually use and believe will help you navigate the crypto markets more effectively. This helps us pay the bills and keep delivering the alpha and market insights you rely on. Thanks for supporting Joined Crypto!

.png)